PJT Partners - An Experiment in Accounting for Advisory Fee Recognition

Synopsis:

PJT Partners is a leading boutique investment bank, providing strategic advisory (M&A), restructuring, and fund placement services to corporations, financial sponsors, and governments. The firm generates the majority of its revenue from advisory fees (~88%), with smaller contributions from placement fees and retainers. These fees are typically calculated as a percentage of transaction value or restructured debt, averaging ~0.5% for deals sized between $1-$5 billion (Aventis Advisors, 2025). Under the current accounting policy, advisory fees are recognized only at deal close, despite work being performed over time. While this complies with GAAP standards and avoids reversals, it causes reported revenues to lag underlying activity, causing revenue volatility. We propose a portfolio-level recognition framework in which PJT recognizes probability-weighted advisory fees ratably over each mandate’s duration, replacing the current all-or-nothing approach. Using a simulated deal backlog, this approach successfully smooths revenues, reducing volatility by ~15 percentage points.

Current Revenue Recognition Policies:

Per PJT’s latest 10-K, revenue recognition follows ASC 606, which requires firms to identify performance obligations within a contract, determine the transaction price, and recognize revenue as those obligations are satisfied. PJT claims that its primary obligation is to “stand ready to perform a broad range of services the client may need over the course of the engagement.” This aligns with the small retainer fees rather than the advisory fees that drive the majority of revenue.

Under ASC 606, advisory fees are recognized only when the transaction price is estimable and the risk of a significant reversal is no longer probable (ASC 606-10-32-5; ASC 606-10-32-11, FASB 2014). This results in “lumpy” revenues, as fees are recorded at deal close rather than over the period in which the advisory work occurs. While retainer fees are recognized ratably, they are economically insignificant relative to advisory fees.

PJT explicitly states the following, indicating that revenues on its income statement lag actual work completed:

The majority of revenues recognized by the Company for the years ended December 31, 2025, 2024 and 2023 were related to performance obligations that were satisfied or partially satisfied in prior periods, primarily due to constraints on variable consideration from prior periods being resolved. (PJT Partners 10-K, 2025)

Current Disclosure Issues:

PJT also elects not to disclose a backlog under ASC 606, providing no visibility into its advisory pipeline (PJT Partners 10-K, 2025). The firm justifies this by noting that obligations exceeding one year are “immaterial,” which is reasonable given that most mandates span less than one year. However, because advisory fees are typically recognized at deal close, revenue is often recorded in subsequent fiscal periods after most of the work is completed. This practice is found consistently across the industry: Houlihan Lokey makes the same election, and Moelis & Company similarly provides no pipeline disclosure.

Proposed Changes:

Part I — Probability-Weighted Ratable Recognition

Alternatively, we propose a two-part framework addressing both revenue recognition and disclosure. Rather than recognizing zero advisory fee revenue until deal close, PJT should recognize a probability-weighted portion of the expected advisory fee ratably over the expected mandate duration. Quarterly revenue should be defined as:

Quarterly Revenue = (Probability(close) x Expected Value(Advisory Fee))/N

where N is the number of quarters from mandate inception to expected close, fixed at inception to preserve ratability.

Under ASC 606, this approach is permissible through the expected value method (ASC 606-10-32-8, FASB 2014), which allows variable consideration as a probability-weighted amount when applied across a portfolio of similar contracts. The variable consideration constraint (ASC 606-10-32-11, FASB 2014) still applies, requiring that recognized revenue be limited to amounts that are unlikely to reverse. Given PJT’s broad mandate base (436 clients in 2025, with advisory fees comprising ~88% of revenue), our probabilistic assumption satisfies this constraint, as expected over and under realizations offset at the portfolio level.

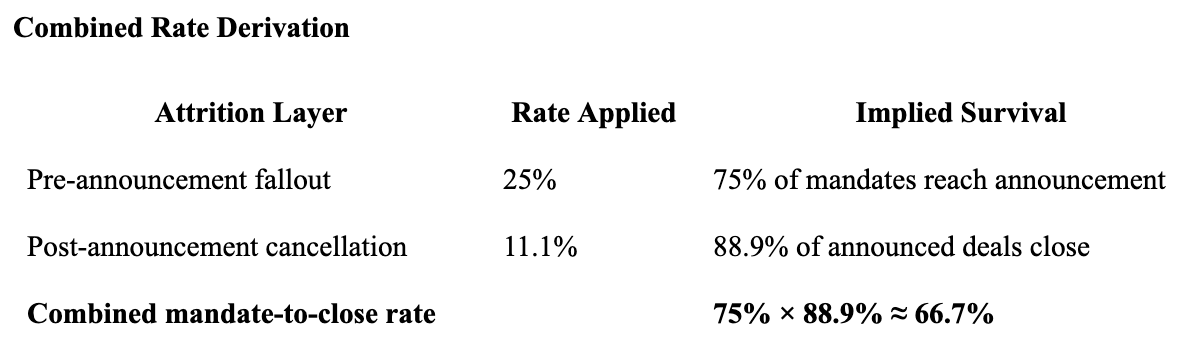

We assume a 65% close probability. Evidence suggests that ~89-90% of announced deals close (McKinsey & Company, 2019); (CFO.com, 2017). Applying an additional conservative 25% haircut for pre-announcement attrition (as we do not have access to this private data) yields a ~66.7% close rate, rounded down to 65% for further conservatism in our model (Aventis Advisors, 2025). Given that elite boutiques are the most coveted advisors and selectively pursue mandates that they believe they’ll win, this likely underestimates realized outcomes.

The remaining 35% is recognized only at close via catch-up. If a deal fails, previously recognized revenue is reversed. However, losses from reversals are limited since only 65% was ever ratably accrued. Over time, catch-ups from successful deals offset reversals, reducing revenue volatility.

Part II — Mandatory Backlog Disclosure

In accordance with the revised recognition framework, PJT should disclose its advisory pipeline in a structured quarterly backlog table, segmented by expected closing horizon. This would provide investors with forward-looking visibility into variable revenues and greater transparency into the timing and derivation of advisory fee recognition. The table would include a realized fee column for closed mandates, reporting actual fees alongside prior estimates in each subsequent quarter, creating a backward-looking accountability mechanism alongside its forward-looking primary function.

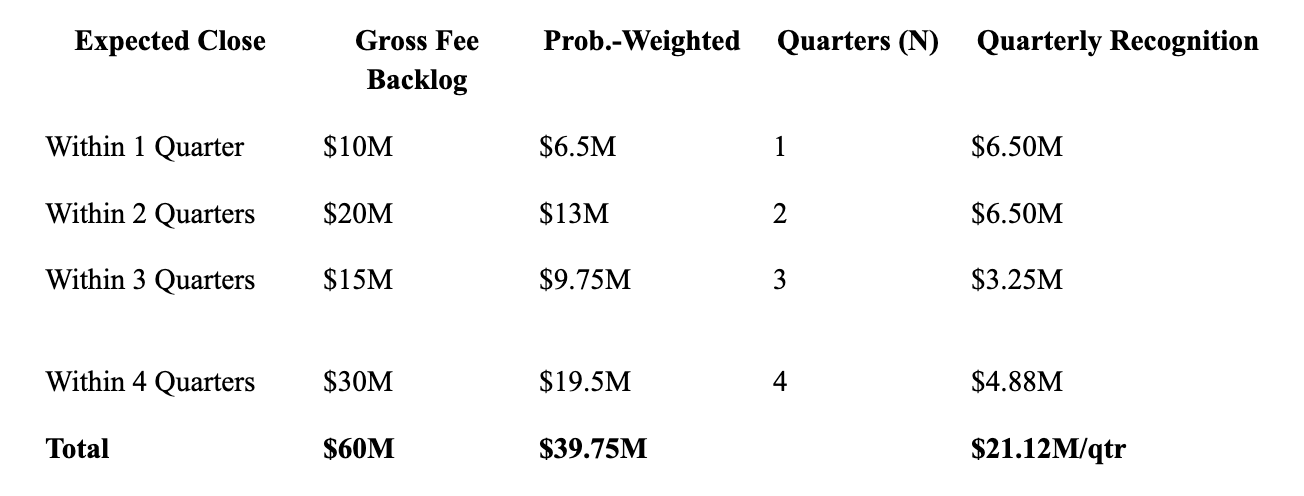

An illustrative disclosure, assuming a 65% close rate applied to a $60 million gross fee backlog, would appear as follows:

This provides investors with a forecast of the pipeline economics driving near-term earnings, the information that PJT’s financials currently lack entirely. The methodology determining the close rate assumption and the expected advisory fee estimates must be disclosed and applied consistently.

The expected advisory fee for any given mandate is estimated as the expected transaction value multiplied by the applicable advisory fee rate, which PJT’s internal preliminary valuations and standard rates determine. Both the individual valuations and fee rate are private to the firm, and thus require no further disclosure to the public. The close rate assumption should be disclosed as a firm-level historical figure, updated annually and subject to audit. This discourages manipulation.

Defense of Current Policy:

While our proposed framework reduces revenue volatility by better accounting for their advisory fees, PJT’s current recognition policy is logical in why they don’t do this. Advisory fees are inherently uncertain and can vary significantly between mandate inception and deal close, driven by factors such as interest rates, market conditions, and investor sentiment. Estimating advisory fees 12-18 months in advance introduces subjectivity and reliance on auditor judgement.

The existing approach, though imperfect, is widely adopted across the advisory industry, allowing for comparability across firms. Recognizing advisory fees at deal close avoids speculative estimates and better reflects the actual cash flows of the firm on the income statement, effectively prioritizing reliability over smoothing.

Results of Policy Change:

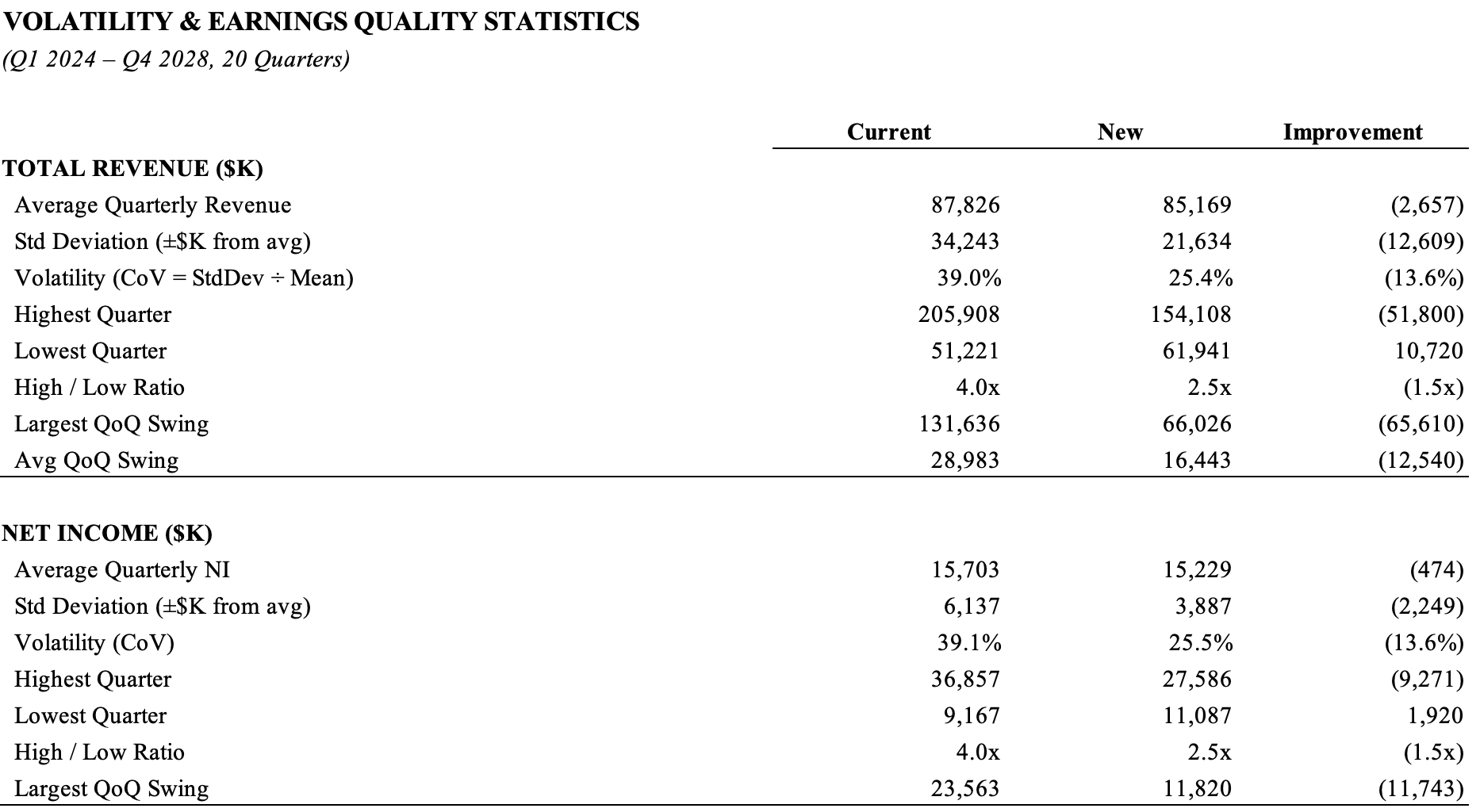

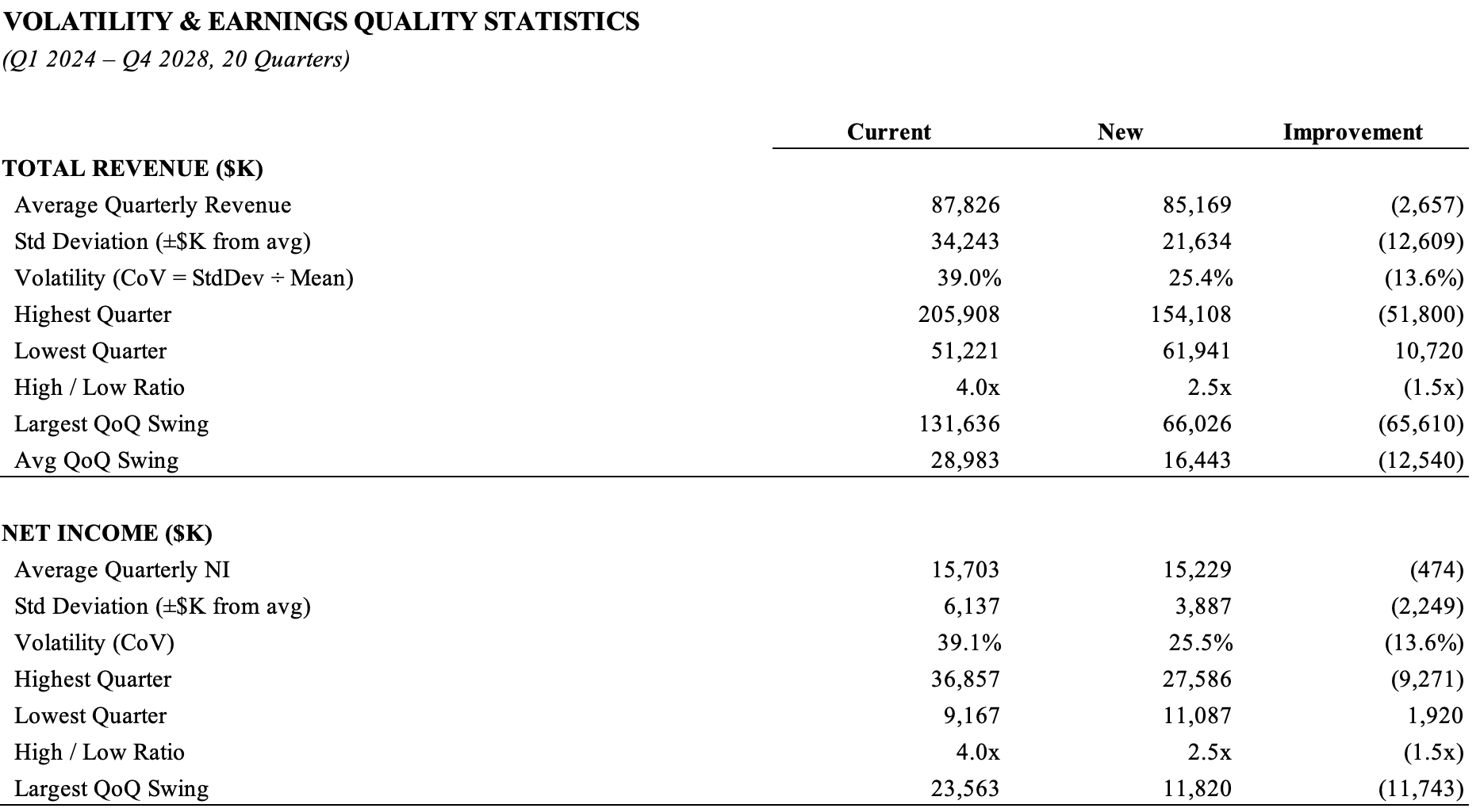

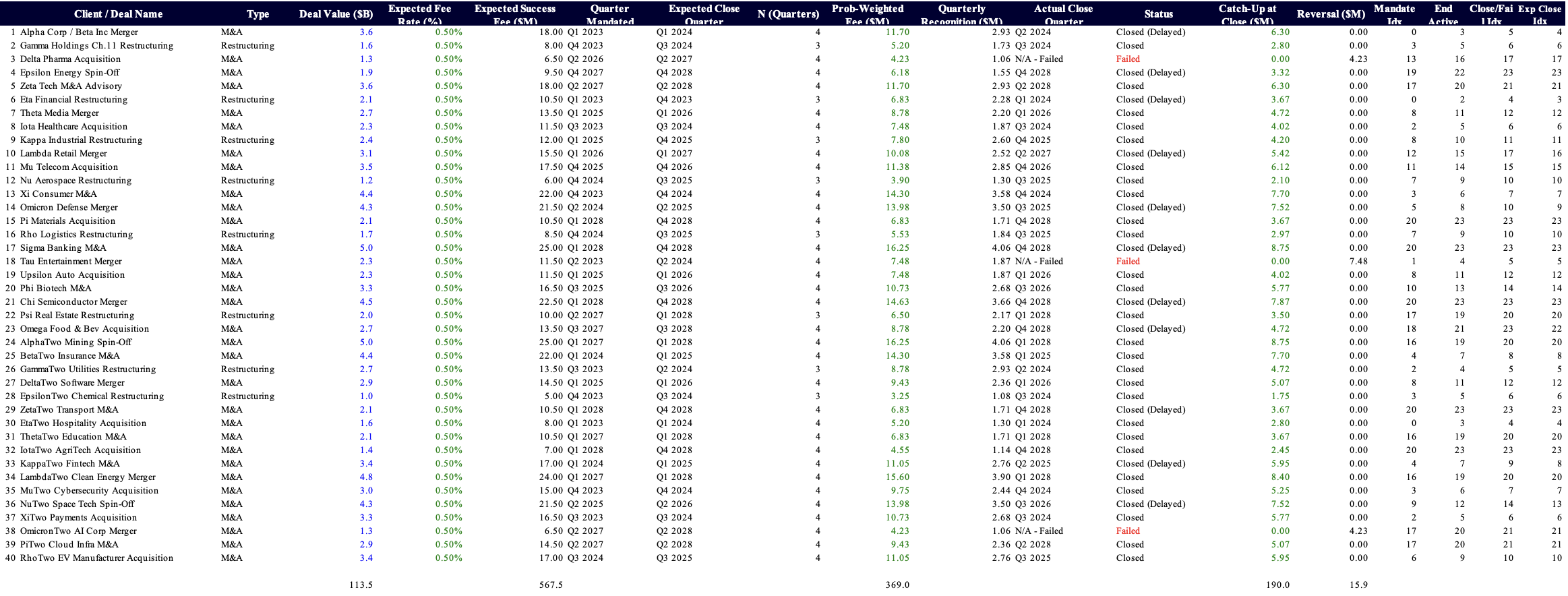

To evaluate the proposed framework, we built a financial model using a simulated deal backlog to generate two sets of financial statements: one under current recognition and one under our probability-weighted ratable approach.

Consistent with our hypothesis, aligning revenue recognition with the timing of advisory work materially reduces revenue volatility. While average quarterly revenues decline by about ~3.0%, volatility falls from ~39% under the current policy to ~25%. Furthermore, the largest quarter-over-quarter revenue swing is reduced by half, from ~$132M to ~$66M. Average quarterly swings also decline from ~$29M to ~16M.

Risks & Mitigants of Proposed Model:

A key risk of the proposed model is reliance on management’s estimates of future transaction values. Since revenue is tied to expected advisory fees, inflating deal values within the backlog would arbitrarily increase current earnings.

For example, PJT could overestimate the value of a $1 billion mandate expected to close in 18 months, particularly during a period of weak deal flow. This would allow the firm to offset a declining backlog by increasing the estimated value of new mandates, effectively smoothing reported earnings through optimistic assumptions while masking the underlying deterioration in deal flow. The duration between mandate inception and deal close creates a window in which inflated estimates are not immediately reconciled with realized advisory fee outcomes, enabling a potential “mark-and-mask” dynamic.

However, this risk is partially mitigated by the catch-up mechanism. Overstated estimates result in smaller or even negative catch-ups at close, making inflation eventually detectable. The critical vulnerability is the detection lag: for an eighteen-month mandate, up to six quarters of inflated revenue could be recognized before any reconciliation occurs, which can mislead an entire earnings cycle. A more murky component is the estimated transaction value assumption, whose underlying methodology and inputs remain private to the firm and are not subject to the same public scrutiny as close-rate assumptions. However, the realized fee reconciliation embedded in the backlog disclosure creates an explicit public track record of estimation accuracy, subjecting management’s valuation assumptions to reputational accountability over time.

Conclusion:

PJT's GAAP-compliant approach delays revenue recognition and limits visibility into its advisory pipeline. Our proposed ratable recognition framework and mandatory backlog disclosure correct both shortcomings, producing financial statements that better reflect economic activity while preserving conservatism.

The most realistic path to implementation is to supplement the current method, rather than replace it. This would leave the existing recognition policy intact while adding our probability-weighted framework as a note disclosure. The supplement preserves cross-firm comparability while equipping investors with a forward-looking signal that PJT’s income statement currently cannot provide.

The industry’s resistance to this type of disclosure is understandable since a shrinking deal backlog does nothing to bolster a firm’s current share price. However, investors’ interests and management’s comfort are rarely aligned. The purpose of financial disclosure is not to protect a firm from an uncomfortable truth, but rather to provide investors the information they need to price that truth accurately. A probability-weighted backlog disclosure would transform an otherwise opaque pipeline into a trackable metric, one that captures both pipeline economics and the accuracy of prior estimates. Investors could begin pricing mandate momentum rather than waiting for the quarterly lumpy surprises.

Firms like PJT Partners are sophisticated enough to manage this disclosure internally. The question is whether they believe their investors deserve to see the same picture management does.

We think they do.

Appendix:

Exhibit 1 - Claude Usage & Prompt to Create Model

I am working on an accounting analysis project for my Financial Reporting and Business Analysis Class. As part of this project, my team needed to critique the accounting method of a firm of our choosing. We chose the advisory investment bank PJT. Part of our analysis requires us to restate the financials of the firm of our choosing (PJT), but based on our new revenue recognition method. Your assignment is to help create an excel model to do this. See the steps below for how I would like you to proceed

1. Read through the file "Accounting Analysis Project Overview" for a general sense of the project

2. Read through the file "Current Write-Up For Claude Modeling Reference" to see our current research, their current revenue recognition method, and our new proposed recognition method. Note that the write-up is not 100% complete

3. Read through the "Write-up scratch sheet" file for further context

4. Read through their 10-k filing in the folder for further context on PJT and specifically their revenue recognition method

5. Go through all of their quarterly reports to create the basic framework for line-items that will be included in the excel model you create. Note you will be creating an income statement and balance sheet (make sure there are correct links between the two financial statements

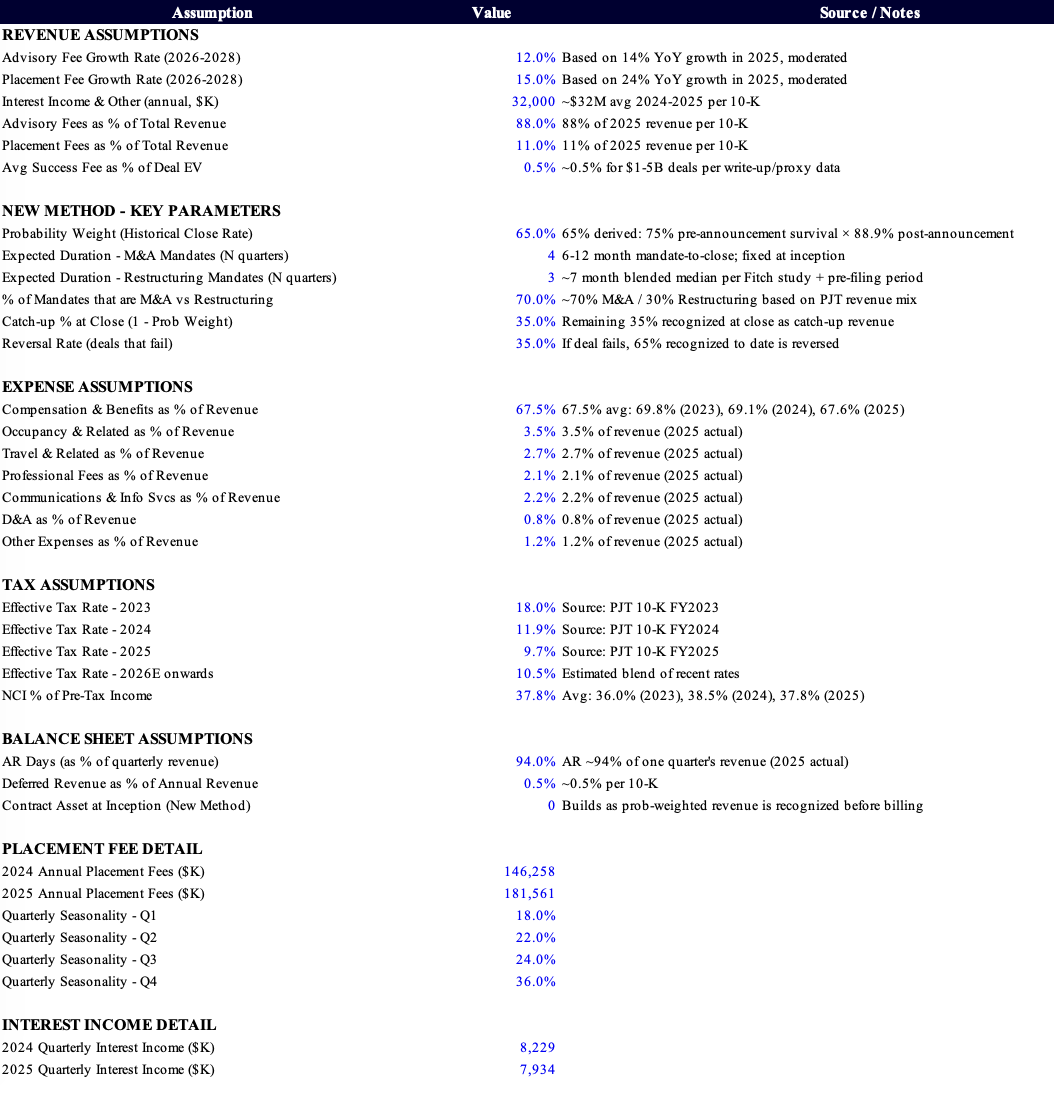

Now we can create the model. Because the current financial statements do not include a backlog that is required, we will need to create two assumption pages. The first will be a base assumption for things like cumulative retainer fees earned in the period (since we will separate this from advisory fees), expense assumptions, taxes (see tax rates from PJT's financial statements). The next will be a theoretical deal backlog page. Here are the formal steps for creating the financial statements

1. Create the general assumptions page

2. create another page with the theoretical deal backlog. Create a random assortment of deals with values ranging from $1 billion to $5 billion scattered across quarters with dates starting at Quarter 1, 2023, all the way to Q4 2028.

3. Create a new page with an income statement and another page with a balance sheet using CURRENT REVENUE RECOGNITION METHODS. Note for the balance sheet you can use actual balances starting at Q1 2023, but make sure any relevant line-item that would change from the theoretical income statement flows.

4. Lastly, create another income statement page and another balance sheet page based off our proposed NEW REVENUE RECOGNITION METHODS

For general formatting, make header pages in navy blue highlight with white text. Make all text in the font Times New Roman. Normal text not in the header can be in black, but make sure to use correct color coding depending on hard codes, references, and formulas

Save the file in the Aiello.Leder folder indexed as "PJT - Revenue Recognition Modeling"

Notes on Claude Usage & Model Prompt:

Claude (Anthropic) was used as an editorial assistant in refining the prose of this write-up. All analytical judgments, arguments, proposed frameworks, and conclusions are the original work of the authors.

An important note on this prompt is that it created the base foundation of the model/simulation of the two accounting recognition policies. Further refining came from our edits and edits from the Claude Excel plug-in, for which there was no export function to all the additional prompts.

Exhibit 2 - Model Excerpt:

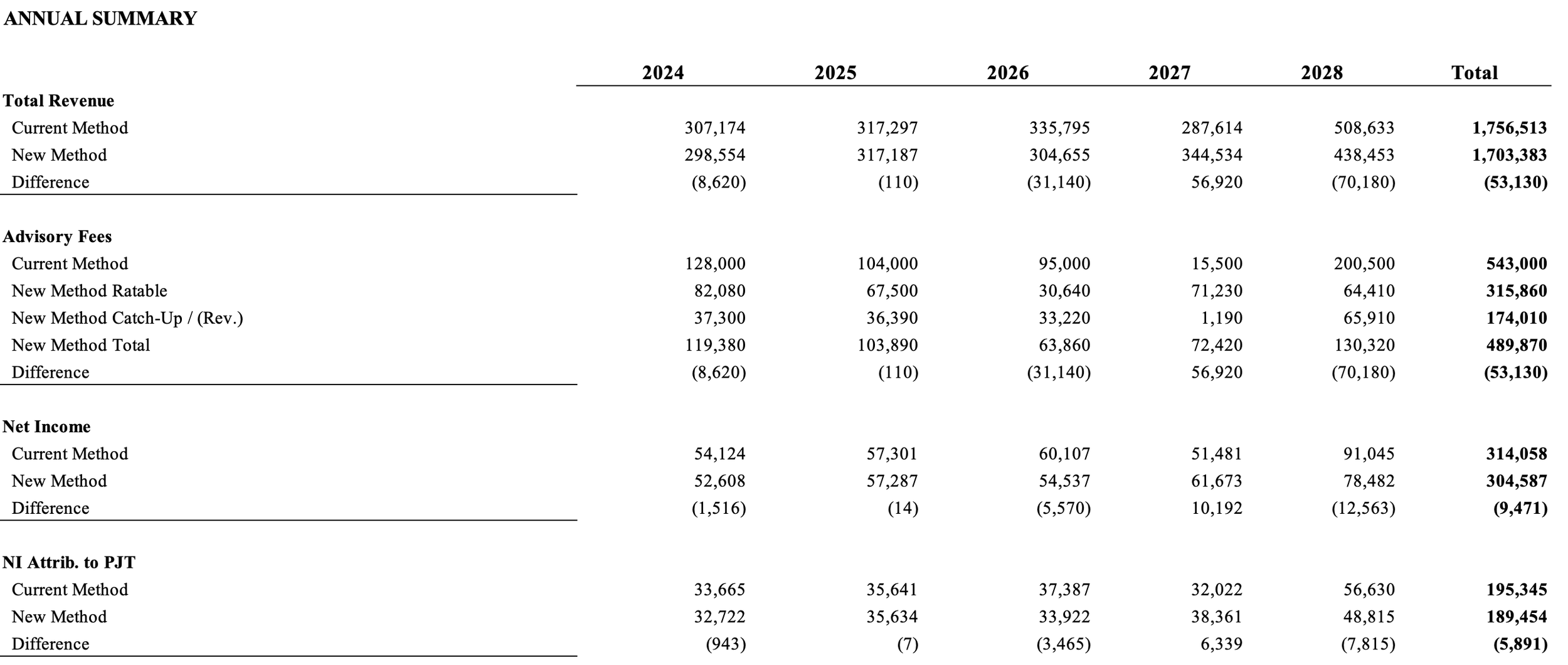

Notes on Model:

Current Method revenue and other earnings are not intended to reflect PJT’s actual revenue and other earnings from the firm’s actual filings. Because PJT does not currently have a deal backlog in their financial statements, for purposes of the simulation, we needed to simulate a theoretical deal backlog that could allow for an accurate comparison between what earnings would be under their current recognition policy versus our proposed policy. The theoretical deal backlog is attached above. Also above is the list of assumptions and estimates we made in our modeling.

Exhibit 3 - Applicable ASC 606 Variable Consideration Rules

The following ASC 606 provisions are referenced throughout this analysis.

ASC 606-10-32-5 — Definition of Variable Consideration Consideration is variable when the amount a company will receive depends on the occurrence or non-occurrence of a future event, including contingencies such as transaction closing.

ASC 606-10-32-8 — Methods for Estimating Variable Consideration An entity must estimate variable consideration using either the most likely amount or the expected value — the sum of probability-weighted amounts across possible outcomes. The expected value method is expressly appropriate when an entity has a large number of contracts with similar characteristics.

ASC 606-10-32-11 — The Variable Consideration Constraint Variable consideration may only be included in the transaction price to the extent it is probable that a significant reversal of cumulative recognized revenue will not occur when the uncertainty is resolved.

ASC 606-10-50-13 — Required Disclosure of Remaining Performance Obligations Companies must disclose the aggregate transaction price allocated to unsatisfied performance obligations and when they expect to recognize it as revenue.

ASC 606-10-50-14 — Practical Expedient Companies are exempt from the ASC 606-10-50-13 disclosure requirement for contracts with an original expected duration of one year or less.

Source: FASB Accounting Standards Codification, ASC 606-10-32 and ASC 606-10-50

Secondary reference: PwC Viewpoint, Section 3.3 — URL: https://viewpoint.pwc.com/dt/us/en/pwc/accounting_guides/health-care/health_care_guide/chapter_3_revenue/3_3_variable.html

Exhibit 4 - Derivation of 65% Probability Weight

The 65% close rate applied in our proposed recognition framework is constructed from two sequential attrition layers, reflecting the two distinct stages at which an advisory mandate can fail to produce an advisory fee.

Layer 1 — Post-Announcement Attrition (Cited Data)

Once a deal is publicly announced, it remains subject to failure from regulatory intervention, financing market disruption, shareholder opposition, or buyer withdrawal. Two large-sample studies establish the failure rate at this stage:

McKinsey & Company analyzed 2,500+ large transactions (>€1 billion) announced between 2013 and 2018 across North America, Europe, Asia-Pacific, Latin America, and the Middle East, finding that approximately 10% of announced deals are canceled before closing.

Source: McKinsey & Company, "Done Deal? Why Many Large Transactions Fail to Cross the Finish Line" (2019)

Cass Business School / IntraLinks analyzed 78,565 transactions globally from 1992 through 2016, finding a failure rate of 11.1% specifically for transactions involving public-company targets — the deal type most representative of PJT's advisory mandate mix.

Source: CFO.com, "Failed M&A Deals Continue to Increase" (2017), citing Cass Business School / IntraLinks study

URL: https://www.cfo.com/news/failed-ma-deals-continue-to-increase/659704/

Applying the public-company-target rate of 11.1% as the more representative figure for PJT's practice, approximately 88.9% of announced mandates close.

Layer 2 — Pre-Announcement Attrition (Estimated)

Advisory mandates are confidential by nature. No academic study or industry data source tracks the rate at which signed mandates fail to reach public announcement. In the absence of published data, we apply a conservative pre-announcement attrition assumption of 25%, consistent with practitioner commentary that a meaningful share of mandates never reach announcement. Aventis Advisors notes that elite advisory firms "typically only take on deals they believe have a high chance of success," suggesting mandate-level close rates at firms like PJT are likely higher than market averages — making our 25% pre-announcement haircut deliberately conservative.

Source: Aventis Advisors, "Understanding M&A Advisor Fee Structures" (2025)

We round down to 65% as a further conservative buffer. The 65% figure is a floor — a higher close rate, which is plausible given PJT's selective mandate engagement, would increase probability-weighted revenue recognized under our framework, strengthening rather than weakening the critique of current treatment.

Note on Restructuring Mandates

The above derivation is calibrated primarily to M&A advisory. Restructuring mandates follow different dynamics — a distressed company retaining PJT is highly likely to complete some form of restructuring process regardless of outcome type. A higher close rate of 75–80% may be more appropriate for restructuring mandates, making our blended 65% rate conservative when applied across PJT's full advisory portfolio.

Exhibit 5 - Derivation of Expected Mandate Duration (N)

N is fixed at mandate inception by deal type and not recalculated as quarters elapse.

M&A Advisory — N = 4 Quarters

Industry sources consistently place the M&A advisory process at six to twelve months from mandate engagement through deal closing. Four quarters represents the upper bound of this range and is applied as a conservative baseline.

Source: Swiecicki Muskett LLC, "How Long Does the Average M&A Deal Take?" (2023)

URL: https://swiecickilaw.com/2023/09/how-long-does-the-average-ma-deal-take/

Quote: "Mergers and Acquisitions deals typically take several months to complete, ranging from six to twelve months or longer."

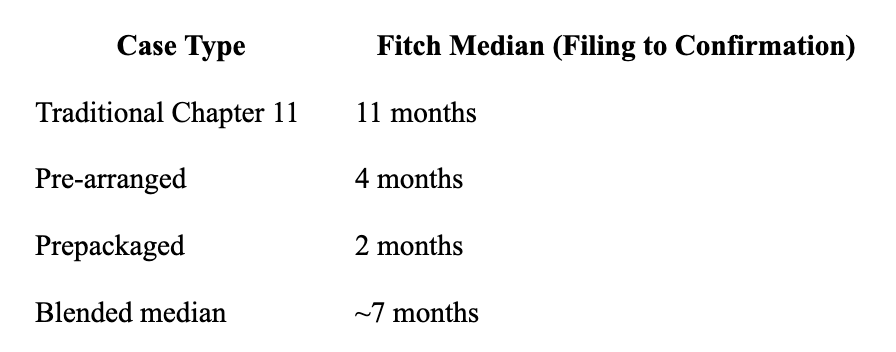

Restructuring Advisory — N = 3 Quarters

Fitch Ratings analyzed 304 U.S. Chapter 11 cases with plans confirmed between 2003 and 2018 across public companies with assets of $500 million to $10 billion, measuring duration from filing through plan confirmation:

Source: Restructuring GlobalView, "The Ever-Shrinking Chapter 11 Case" citing Fitch Ratings, "Shrinking Length of U.S. Bankruptcies" (August 2018)

URL: https://www.restructuring-globalview.com/2018/08/the-ever-shrinking-chapter-11-case/

The blended median of approximately seven months, combined with a typical pre-filing retention period of four to six weeks during which advisors are engaged before any bankruptcy proceeding begins, produces a total mandate duration approaching but not exceeding three quarters. N = 3 is therefore the appropriate assumption for restructuring engagements. Note that traditional Chapter 11 mandates — PJT's most complex and highest-fee restructuring engagements — carry an eleven-month in-court median alone, meaning N = 3 is a conservative floor for that subset.

Exhibit 6 - Illustrative Journal Entries Under Proposed Framework

The following entries illustrate the accounting treatment for a $1,000,000 expected advisory fee under the proposed framework, assuming a 65% close rate and N = 4 quarters, with quarterly recognition of $162,500.

Each quarter during engagement:

Dr. Contract Asset 162,500

Cr. Advisory Revenue 162,500

At deal close — actual fee equals estimate ($1,000,000):

Dr. Accounts Receivable 1,000,000

Cr. Contract Asset 650,000

Cr. Advisory Revenue 350,000

Dr. Cash 1,000,000

Cr. Accounts Receivable 1,000,000

At deal close — actual fee exceeds estimate ($1,100,000):

Dr. Accounts Receivable 1,100,000

Cr. Contract Asset 650,000

Cr. Advisory Revenue 450,000

At deal close — actual fee below estimate ($900,000):

Dr. Accounts Receivable 900,000

Cr. Contract Asset 650,000

Cr. Advisory Revenue 250,000

Net advisory revenue in closing quarter = $250,000.

Deal falls through after three quarters of recognition ($487,500 recognized at date of deal fall through):

Dr. Advisory Revenue 487,500

Cr. Contract Asset 487,500

Since only 65% × ¾ was ever recognized, the reversal is $487,500 rather than the $1,000,000 that would have been recognized under a 100% approach, demonstrating the conservatism built into the framework. Even if revenue from this deal was reversed, offsetting catch-ups for other successfully closed deals across the portfolio would likely mitigate the effects of this reversal, allowing for smoother earnings.